Inhalt

Michael Raber

CEO

Your specialist for IT consulting and support.

CSRD EU Sustainability Directive – What to do?

The EU’s CSRD (Corporate Sustainability Reporting Directive) poses challenges for companies, but if approached correctly and pragmatically, they can be reasonably solved even for medium-sized companies and even SMEs. After all, it is also in the interest of the company to act sustainably. What is a necessary evil in the short term will certainly turn into a competitive advantage in the medium term.

The following article clarifies the most important questions regarding CSRD. In this context, the term ESG (Environmental, Social, Governance) is also used in some cases. Ultimately, however, it is first important to understand the context and both terms basically describe the same guideline.

What means ESG or CSRD?

CSRD stands for Corporate Sustainability Reporting Directive – in other words, a report on the sustainability of the company. ESG stands for Environment, Social Responsibility and Governance. However, both go in the same direction: companies are to be obliged not only to deliver products and financial reports according to certain standards, but also to ensure the sustainability of the entire company at the same time – and to report on this as well. CSRD reporting is the same as financial reporting and must meet certain standards.

Who is affected by ESG reporting?

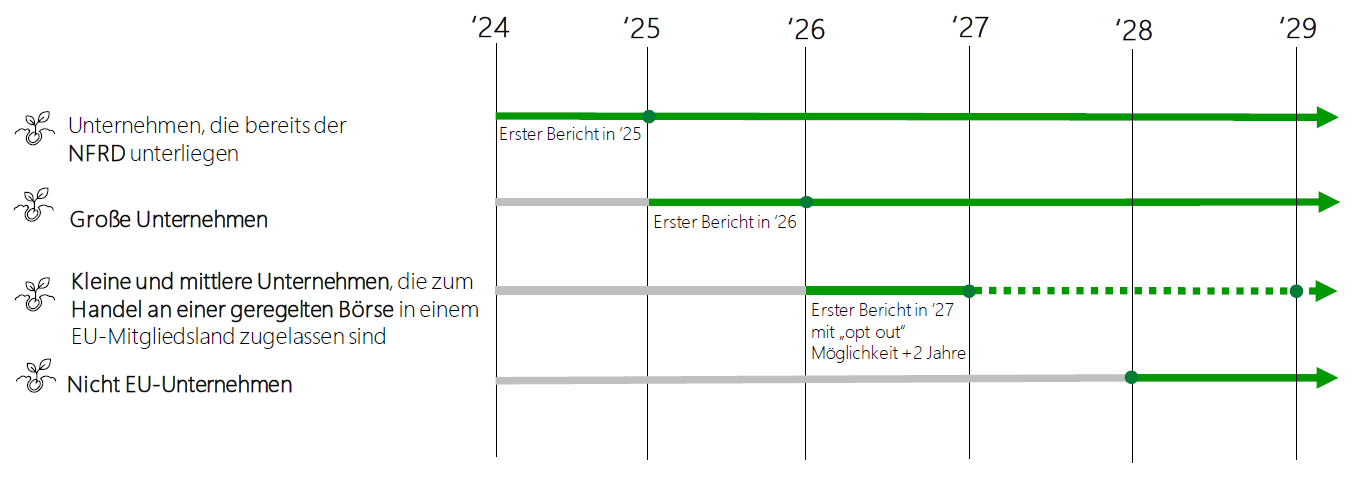

Basically, it can be said that every company is affected – at some point. Initially, it affects large corporations and companies listed on the stock exchange. Per CSRD, the individual phases are defined as follows.

©2023 HYPT: From when do companies have to report?

Even though changes may still be pending here, sooner or later every company will be confronted with it, and ideally also benefit from it.

Where does the data come from? Know exactly or estimate?

As already outlined above, data from many different areas come into play. How exactly this data is collected depends on the company and the industry. Manufacturing companies with high energy consumption (e.g., foundries) have a different focus than automotive suppliers who, for example, also receive specific specifications from their customers. Or companies with a large fleet may want to track vehicle data, such as mileage and consumption, in more detail. So you have to look at each company individually and consider which data can be determined by a rough estimate and where detailed recording makes sense.

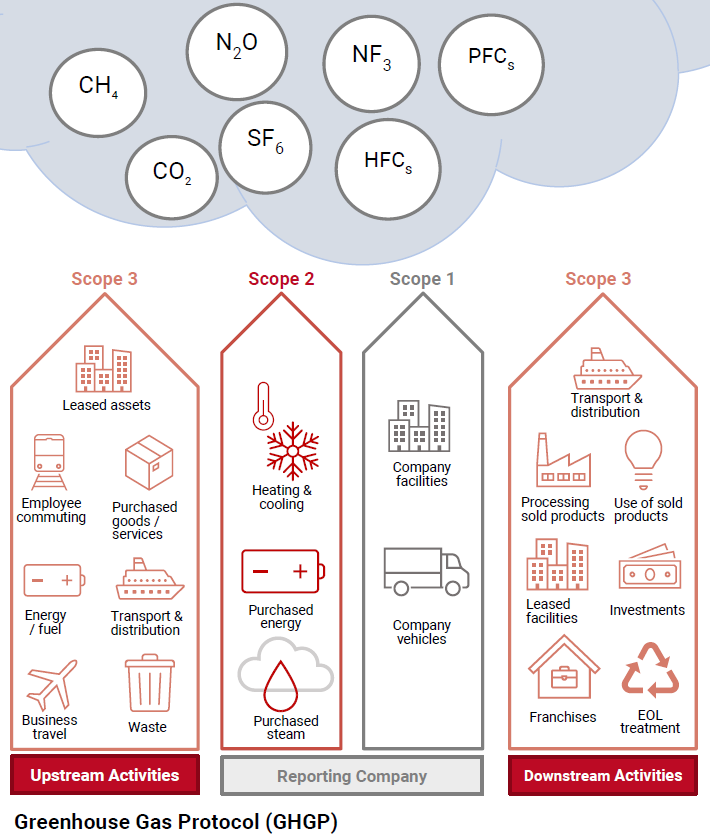

Basically CSRD is divided in different sections, called Scopes:

Scope 1 are direct impacts of the company on climate change that occur during production.

Scope 2 are indirect influences of the company that arise from purchased energy, materials, etc.. This quickly makes it clear that suppliers also come into play here.

Scope 3 goes much further. Here, all upstream and downstream processes are taken into account. Even the energy consumption of the goods produced in the product life cycle must be taken into account.

Is the ERP system important as a data source?

The ERP system is the central data repository in many companies. Here you can find supplier and order information, product data, manufacturing processes, sales and shipping data and much more, which is important for CSRD reporting depending on the company and industry. In this respect, the ERP system is set as the data source in most cases. The advantage is that current and reliable data can usually be found in the ERP system, since this is where the operational business is mapped. The only thing that needs to be taken care of here is access to the data, but this should not be a problem with modern ERP systems.

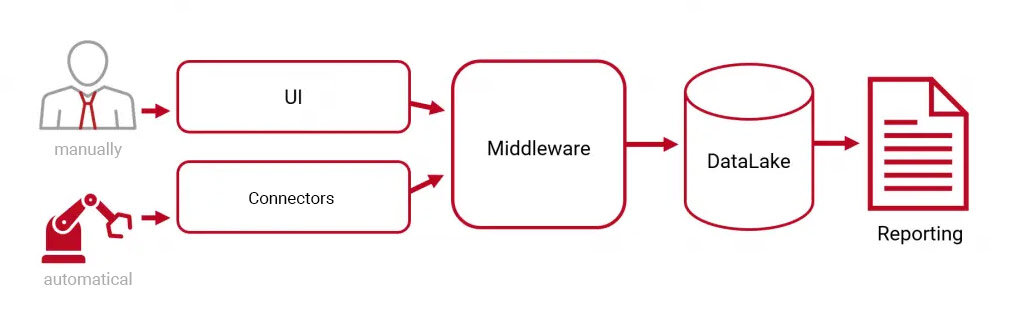

How does the infrastructure need to work in order to efficiently process CSRD-relevant data?

As already mentioned the data must converge in one place in order to be reused for reporting. In contrast to structured company data, such as that managed in ERP systems, only an unstructured database can be used for CSRD reporting, since a large number of different data structures have to be recorded. A standard SQL database would quickly reach its limits here. Basically, we have the following components here:

Goal setting and tracking in CSRD – where is the journey heading?

In principle, CSRD reporting should not be reduced to compliance with legal requirements. The data, such as energy and resource consumption, can help to evaluate the success of optimization measures. For this purpose, one should define one’s own objectives and measure the success with the help of the CSRD report. The resulting data can also be used as a basis for corporate decisions on efficiency and cost reduction.

How to approach CSRD pragmatically now?

Here are two areas to think about:

Technology: the collection of data must be implemented with an appropriate concept. The above-mentioned components UI, middleware, DataLake and reporting should ideally be created from a single mold. If we work with many different technologies and concepts here, this will become a problem in the medium term. The setup should therefore be thoroughly thought through before the start and, if necessary, implemented with external help.

Organisation: There is also a lot to be done organizationally. An individual objective and the necessary procedure must be defined. In the next step, this is then set up as a project – with a corresponding backward timeline. The most important question that arises here is whether this can be done in-house by an employee with the appropriate training and experience, and whether this employee also has the necessary time to devote to it intensively. An alternative is an externally contracted specialist who, together with you and your employees, collects the required data, analyzes it and transfers it into a CSRD report. The goal: a lean approach to sustainability reporting for medium-sized companies.